I’m back with another instalment of Freelance Finance! Last time, we explored bookkeeping methods to keep track of your income. And in this post, we’ll look at a system that will help organise your money and build a financial safety net.

Like last time, these posts are intended for beginners, and should not be taken as absolute advice but an introduction to some concepts that I have personally found useful.

The Bookeeper, 1901 – H.O. Kennedy

The Bucket Method Explained

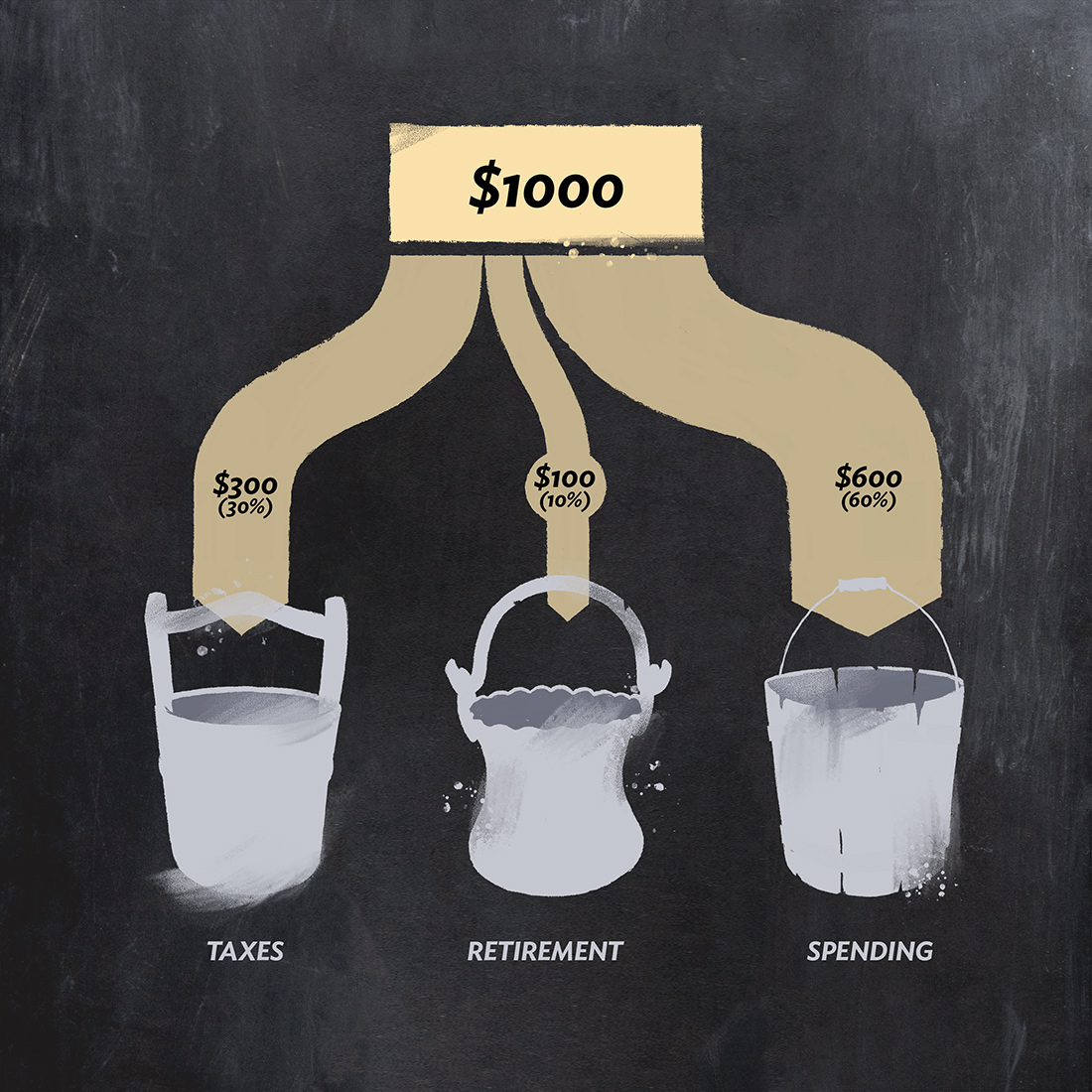

The bucket method involves splitting your money into categories or “buckets” based on specific financial needs. You then divide each incoming payment you receive into these buckets proportionally. A bucket is typically a bank account, but can also be things like a retirement fund or investment. Here is an example of a simple bucket setup:

In this example, you are paid $1000, of which 30% is put into a tax bucket, and 10% into a retirement bucket, leaving $600 for spending. You decide the number of buckets and contribution percentages based on your monthly expenses and financial goals.

This may seem obvious, and no different to… well, just saving money. But I have found that setting up a system of buckets and splitting up every pay makes things more organised, and allows me to save for different goals at the same time.

I first encountered this concept in a book called The Barefoot Investor by Scott Pape, which is a great read for beginners to personal finance (though the book has an Australian focus, so may not be relevant to those living elsewhere). The method described in the book is aimed at people with consistent incomes, but I’ve adapted it here for freelancers.

The Farmer’s daughter – John Everett Millais

Potential Buckets

Here are some potential buckets you may want to have:

Taxes (a must for freelancers!)

‣ Contribute into this bucket a percentage based on your estimated taxes.

‣ If you round up the percentage, you end up with a little extra at the end of the year, which covers any unforeseen taxes, or becomes a nice end of year bonus!

Emergencies

‣ Use this bucket for things like repairs or unexpected bills.

‣ Also covers lean times, or if you cannot work due to illness/injury.

‣ Aim to keep 3 to 6 months of living expenses for a solid financial safety net.

‣ Some buckets (like this one) can have a finite amount; contribute into it until you reach a specific sum, and only top up if you take money out.

Retirement

‣ The earlier you start a retirement fund the better; compound interest is your friend!

‣ Depending on your location, you may get significant tax breaks for contributing to a retirement fund.

Long Term Savings

‣ It’s important to save towards things that set you up for a better future!

‣ This bucket does not need to be a bank account, and could be some form of long term investment that will grow over an extended period of time.

Short term savings

‣ You can use buckets to save for relatively smaller (but expensive) things too; anywhere from art workshops to a holiday.

‣ Keep this bucket separate from long term savings, so that you can set distinct short and long term financial goals.

Fun

‣ Guilt free spending! Because you deserve a treat!

‣ You can either set a finite amount for this bucket to prevent overspending, or contribute a % of each pay.

Spending

‣ This is not a true bucket, as it is the bank account that you are paid into. After dividing your pay into other buckets, what remains is your spending money.

‣ Through working out your monthly budget, you can estimate how much you’ll need in this spending bucket. Any extra funds can go into savings or a surplus bucket (see below).

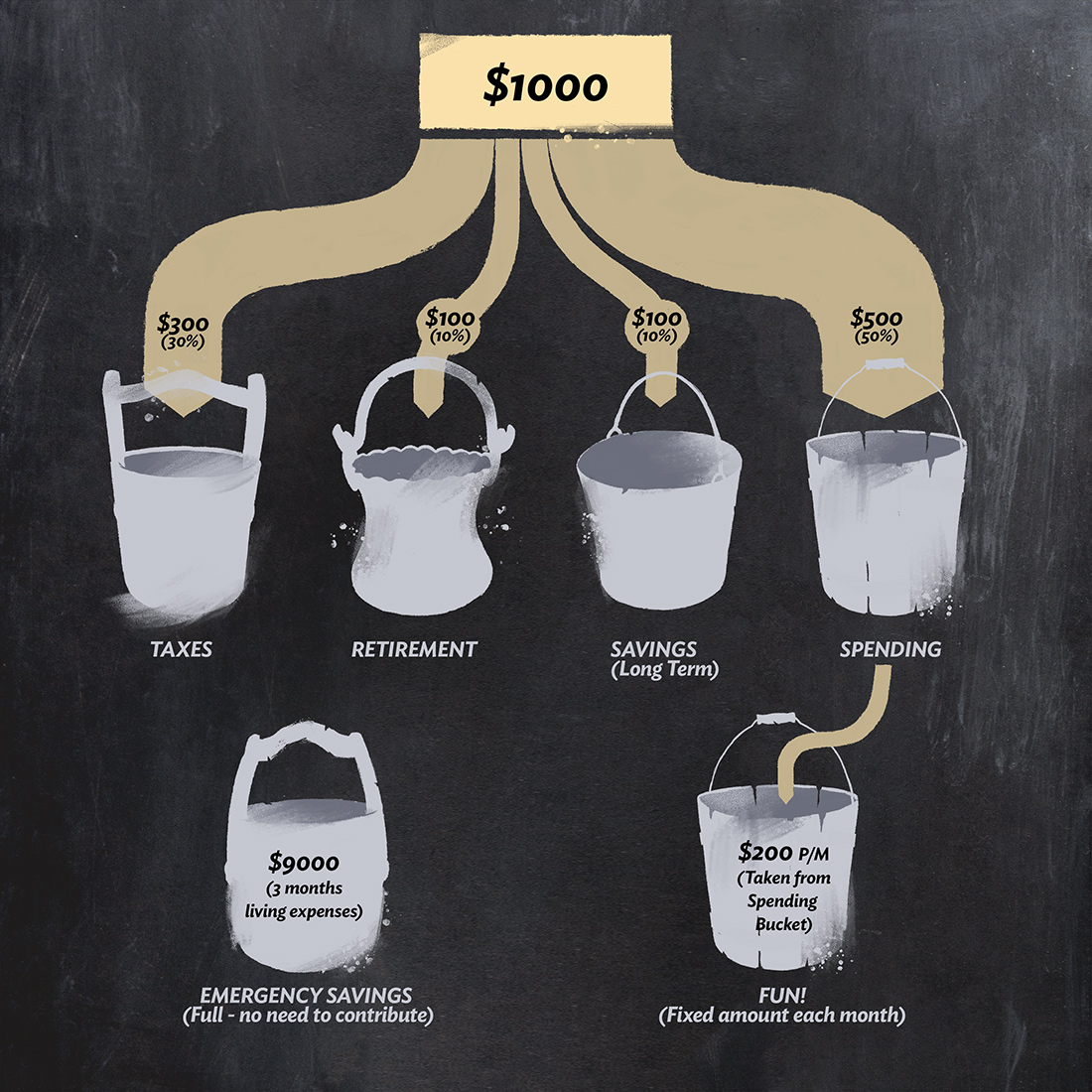

Now that we’ve covered some bucket possibilities, here is an example of how a more complex bucket setup might look:

If this feels too complex, you can start with fewer buckets that align most closely with your financial goals. You also don’t need to contribute large percentages as shown here. If your living expenses take up a significant amount of your pay, putting away even 2% of your income towards an important bucket like retirement or emergencies can be useful, and will set you up with the infrastructure to contribute more when you’re able.

Though the idea is to split every incoming payment, I simplify the amount of maths and transferring I do by grouping payments into bundles. I tally up all my payments every 2-4 weeks, and do one transfer proportionally into all my buckets.

Danaides – John William Waterhouse

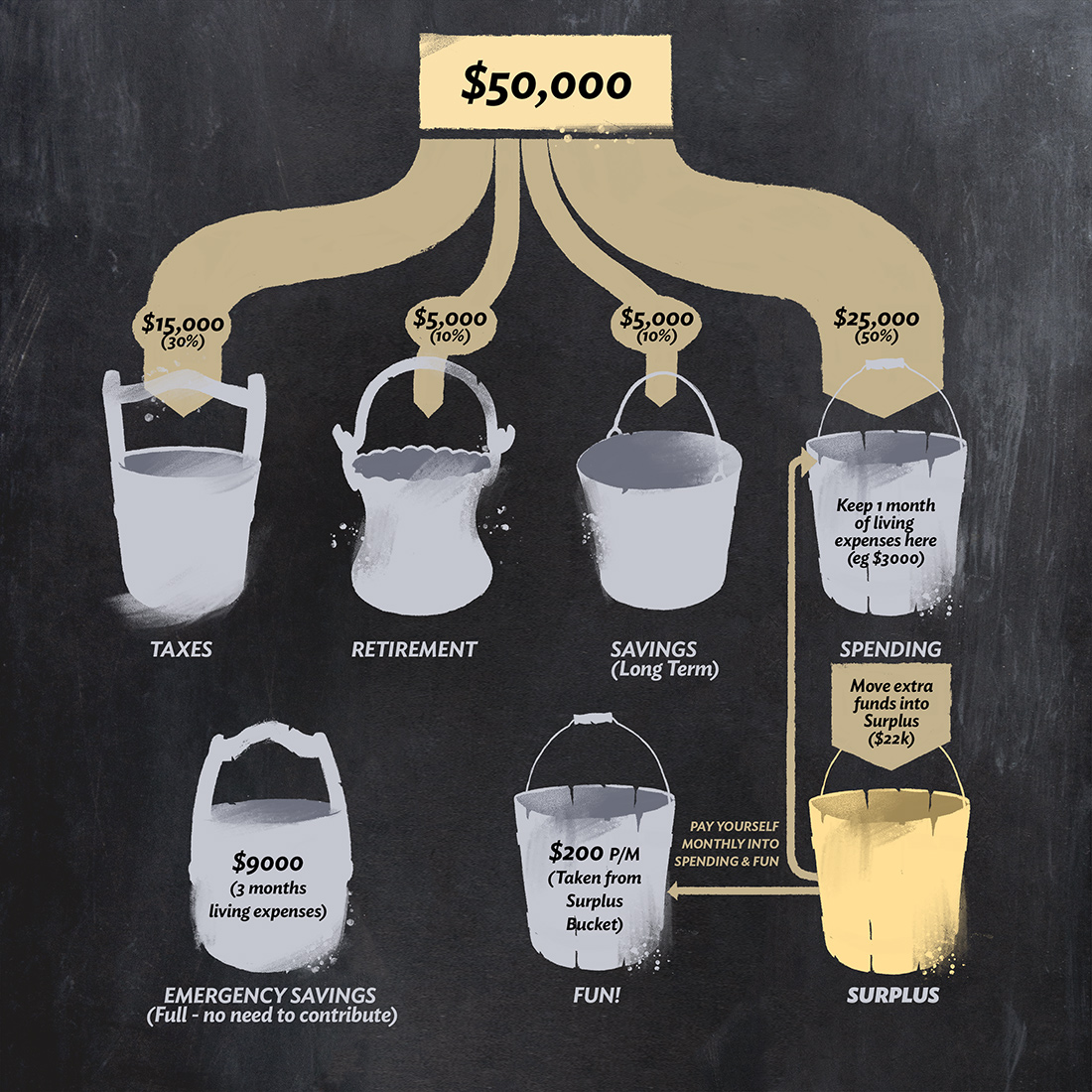

The Golden Surplus Bucket

There is one last bucket that is especially useful for freelancers: the surplus bucket. This bucket will address the problem of irregular payments; where you receive large payments in some moths but none in others.

When you receive a large payment, divide it among your buckets like normal. Then, if a significant amount of spending money remains, put it in a surplus bucket from which you pay yourself a monthly “wage”. An example of this in action:

In this example, you receive a payment of $50,000, and it is split into buckets as planned. This leaves $25,000 in spending money. Looking at this sum, you might be tempted to splurge! BUT, if this payment was something like a picture book advance, you will need it to last for several months as you work on said project. So here’s where the surplus bucket comes in; you keep 1 month of living expenses in your spending bucket (in this example, $3,000), and move the extra into surplus. Then use this surplus to pay yourself every month into your spending (and fun) buckets. Over time, in the happy event you notice this bucket filling up, and you anticipate more funds imminently, you can move some of the excess into one of your savings buckets – bonus savings!

Cover for the Saturday Evening Post – JC Leyendecker

Parting Thoughts

The bucket method is a practical way to organise money, and over time it can help you build a strong financial safety net. One area I’ve been vague about here is the percentages you should contribute into each bucket, as this requires a closer look at budgeting. Additionally there are numerous other ideas to explore, like how to invest and grow some of these funds, instead of sitting on them in a bank account like Smaug atop a pile of treasure — but we’ll cover these in future posts!

Conversation with Smaug – J.R.R. Tolkien

This post is part of a Freelance Finance series:

1 – Bookeeping

2 – Buckets (You are here)

3 – Budgeting

{kind=link}

Thanks Rovina, these are excellent nicely explained art business concepts. I would like to emphasize the bucket for retirement, which is particularly important for freelancers. Over the years in my career as a freelance visual effects artist and animator, I DID save the max allowed in an IRA each year, which also helps save on taxes. I am doing fine in retirement as a result, however I have many artist friends who apparently did not save and are really struggling financially once they became seniors and couldn’t get gigs anymore!

Save as much as possible in an IRA, and put it in a S&P 500 index fund or equivalent. Let compounding interest and dividends be your friend in your senior years.

she’s been laid off for two months, the previous month her paycheck was $20328 ONLY working at home for a couple of hours each day… check out…

www.pays77.com

Thanks for this series!

What are the key strategies for effectively managing finances as a freelance worker, as discussed in the article “Freelance Finance Buckets”?

Thanks for sharing your insights on freelance finance and introducing the concept of “buckets”! It’s crucial for freelancers to manage their finances effectively, and exploring innovative solutions like the one you’ve suggested can be immensely beneficial.

Exploring platforms like ICOHolder can offer valuable insights and resources for those interested in navigating the NFT space. From tracking the latest trends to gaining a deeper understanding of the potential implications for freelance finance, leveraging such platforms can be instrumental in staying informed and making informed decisions.

Managing payments effectively is a cornerstone of any successful business, and I’ve found a platform that excels in this area. With its secure transaction processing and user-friendly interface, it has simplified my operations significantly. The ability to monitor transactions in real-time and access detailed analytics has been particularly beneficial. For those in need of a robust payment gateway, I suggest exploring transferty for its comprehensive features.